Statistical Notes Friday September 30

-Initial unemployment claims in the United States fell significantly in the latest week, though that may have been largely due to seasonal adjustment problems.

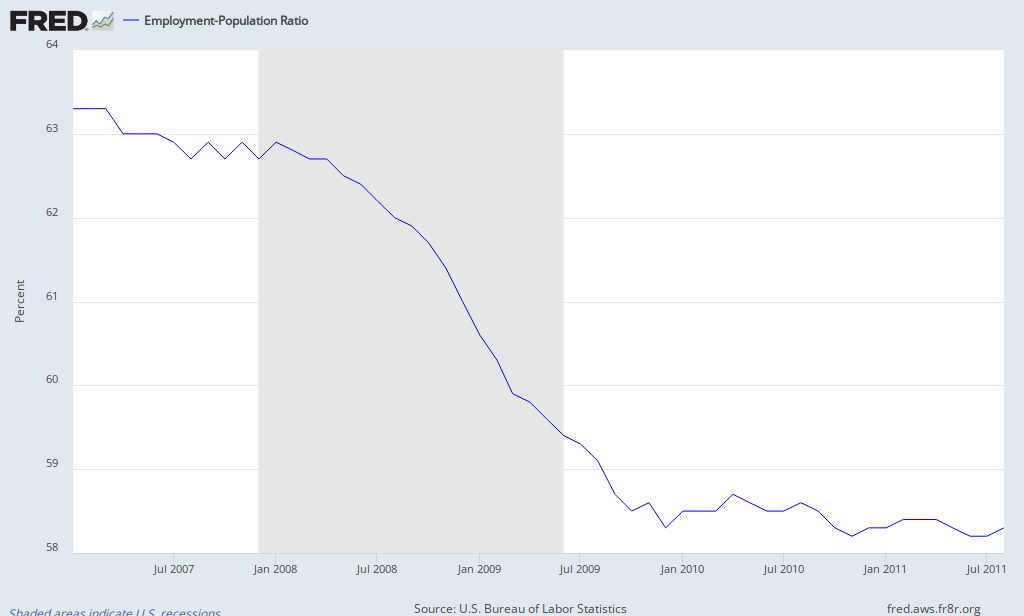

Real personal income fell in August by 0.3%, the second monthly drop in a row, while spending was unchanged, causing the savings rate to drop to 4.5%, the lowest since November 2009.

Meanwhile, second quarter GDP was upwardly revised while GDI was downwardly revised.

-Monthly GDP in Canada rose 0.3% in July, following a 0.2% gain in June.

-Preliminary September euro area inflation rose to 3.0% from 2.5%, reducing the probabilty of an ECB interest rate cut.

-The employment rate in Germany rose while unemployment rate fell in August. During the latest year the employment rate has risen from 61.9% to 63% while the unemployment rate has dropped from 6.9% to 6%.

-Real retail sales in Latvia rose in August rose by 1.6% compared to July and 7.4% compared to August 2010.

In Estonia, real retail sales fell by 1% in August compared to July, but rose 4% compared to August 2010. Industrial production fell by 1.8% compared to the previous month but rose 22.7% compared to a year earlier.

-Household spending in Japan fell by 2.8% compared to a year earlier, and employment also fell. Industrial production however rose, but less than expected.

Real personal income fell in August by 0.3%, the second monthly drop in a row, while spending was unchanged, causing the savings rate to drop to 4.5%, the lowest since November 2009.

Meanwhile, second quarter GDP was upwardly revised while GDI was downwardly revised.

-Monthly GDP in Canada rose 0.3% in July, following a 0.2% gain in June.

-Preliminary September euro area inflation rose to 3.0% from 2.5%, reducing the probabilty of an ECB interest rate cut.

-The employment rate in Germany rose while unemployment rate fell in August. During the latest year the employment rate has risen from 61.9% to 63% while the unemployment rate has dropped from 6.9% to 6%.

-Real retail sales in Latvia rose in August rose by 1.6% compared to July and 7.4% compared to August 2010.

In Estonia, real retail sales fell by 1% in August compared to July, but rose 4% compared to August 2010. Industrial production fell by 1.8% compared to the previous month but rose 22.7% compared to a year earlier.

-Household spending in Japan fell by 2.8% compared to a year earlier, and employment also fell. Industrial production however rose, but less than expected.

posted by stefankarlsson at 3:05 PM

0 comments

![]()

![]()