Greg Mankiw On Real Bond Yields

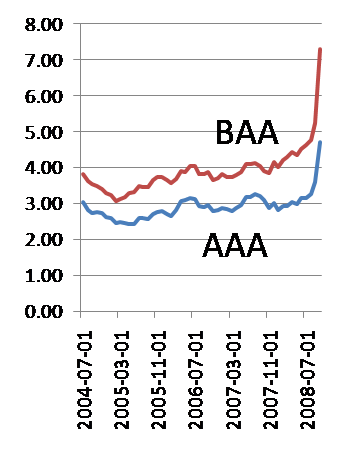

A reader asked me to comment on this post from Greg Mankiw, which was based on a post from Paul Krugman where the below chart appeared.

Apparently Krugman has calculated this by taking the nominal yields of AAA and BAA-rated corporate bonds and from that subtracting the differential between regular and inflation-protected 20-year government bonds. This increase in yields is to only a small extent the result of an increase in nominal yields with regards to AAA-rated bonds, while being to a larger extent the result of rising yields with regard to the BAA-rated bonds. The fact that corporate bond yields in general and BAA-rated ones in particular are up even as government bond yields are down clearly reflect an increase in risk premiums.

The increase is however also the result of a decline in the differential in between regular and inflation-protected bonds. For AAA-rated bonds, the decline in the differential between regular and inflation-protected bonds are more important than the increase in the nominal yield, while for BAA-rated bonds, the increase in nominal yields are more important.

Mankiw therefore proposes an inflation target as a remedy to this. With an inflation target, the differential in yield between regular and inflation-protected bonds will go up and so supposedly push down the real corporate bond yields.

But there are several problems with this. First of all, it is not even certain that the increase in yield differential between regular and inflation-protected bonds even reflects lower inflationary expectations. It probably does to some extent, but it also likely reflect a higher liquidity premium for the less liquid inflation-protected series. Secondly, inflation targets will have no effect on the increase in risk premiums which explain much of the increase. Thirdly, is there really anyone who doubts that the Fed is doing everything they can to inflate? The Fed has historically created a lot more inflation than other advanced country central banks without an inflation target and given the dramatic increase in the size of the Fed balance sheet, there can be little doubt that they are trying to reignite inflation. One can debate whether or not they will succeed, but as it is clear that they are trying, an inflation target wouldn't make any difference. And finally, since nominal yields are significantly above zero, an increase in inflationary expectations wouldn't push down real yields, it would only increase nominal yields.

Apparently Krugman has calculated this by taking the nominal yields of AAA and BAA-rated corporate bonds and from that subtracting the differential between regular and inflation-protected 20-year government bonds. This increase in yields is to only a small extent the result of an increase in nominal yields with regards to AAA-rated bonds, while being to a larger extent the result of rising yields with regard to the BAA-rated bonds. The fact that corporate bond yields in general and BAA-rated ones in particular are up even as government bond yields are down clearly reflect an increase in risk premiums.

The increase is however also the result of a decline in the differential in between regular and inflation-protected bonds. For AAA-rated bonds, the decline in the differential between regular and inflation-protected bonds are more important than the increase in the nominal yield, while for BAA-rated bonds, the increase in nominal yields are more important.

Mankiw therefore proposes an inflation target as a remedy to this. With an inflation target, the differential in yield between regular and inflation-protected bonds will go up and so supposedly push down the real corporate bond yields.

But there are several problems with this. First of all, it is not even certain that the increase in yield differential between regular and inflation-protected bonds even reflects lower inflationary expectations. It probably does to some extent, but it also likely reflect a higher liquidity premium for the less liquid inflation-protected series. Secondly, inflation targets will have no effect on the increase in risk premiums which explain much of the increase. Thirdly, is there really anyone who doubts that the Fed is doing everything they can to inflate? The Fed has historically created a lot more inflation than other advanced country central banks without an inflation target and given the dramatic increase in the size of the Fed balance sheet, there can be little doubt that they are trying to reignite inflation. One can debate whether or not they will succeed, but as it is clear that they are trying, an inflation target wouldn't make any difference. And finally, since nominal yields are significantly above zero, an increase in inflationary expectations wouldn't push down real yields, it would only increase nominal yields.

posted by stefankarlsson at 4:44 PM

![]()

![]()

2 Comments:

Hi Stefan:

Great post. Definitely clarified the issue. Thanks.

The most compelling point you make is the last one -- the fed is already doing everything it can to inflate, so it's true that it's hard to see what more they can do. Bernanke has declared many times -- he will do everything in his power to prevent deflation.

: )

Post a Comment

<< Home